Directors Databank (Empannel Yourself)

Directors Databank (Empannel Yourself)

Become a faculty

Become a faculty

Blog

Blog

Become an Awards Assessor

Become an Awards Assessor

Publications

Publications

Contact Us

Contact Us

What do you feel are some of the factors/ pressures that can contribute to frauds in the future?

Has the Audit Committee of your board established an effective anti-fraud (including Financial Statement Frauds) and misconduct detection mechanism?

Do you believe independent directors can play a significant role in preventing, detecting and responding to fraud?

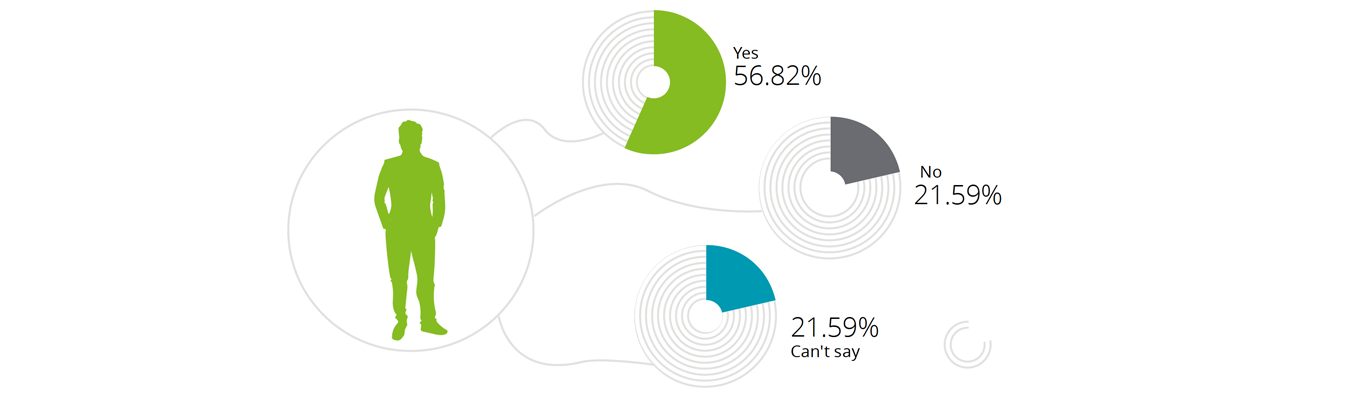

Would you choose to be a part of a board that has previously reported/ experienced fraud?

Amidst uncertain times that corporates are facing today due to COVID-19, IDs need to act with the highest standards of vigilance and prudence. While the accountability and expectation of IDs in consideration of past corporate scandals/failures have considerably increased over the past few years, regulators are also mindful of the limitation and challenges IDs face as part of their fiduciary responsibilities4. In this context, the Ministry of Corporate Affairs (‘MCA’) issued a clarification on 2 March, 2020 declaring that prosecution proceedings will not be initiated against independent and non-executive directors (‘NEDs’) unless there is sufficient evidence to prove that such default or violation had been committed with their knowledge or consent or they were guilty of gross and wilful negligence or fraud. To fulfil regulatory obligations and meet stakeholders’ expectations, IDs could consider the following measures:

Quick Links

Quick Links

Connect us

Connect us