Quick Links

Quick Links

Connect us

Connect us

Directors Databank (Empannel Yourself)

Directors Databank (Empannel Yourself)

Become a

Become a  Become a

Become a  Blog

Blog

Become an Awards Assessor

Become an Awards Assessor

Publications

Publications

Contact Us

Contact Us

What Powers Organisational Culture and Performance? The Third-Team

What holds a board back from being truly effective? What stops a board from influencing executive performance which, in turn, affects organisational performance? Is it the board alone or an amalgamation of the board and executive that drives effectiveness and organisational performance? How do we measure this? These are questions I am asked most often in my advisory practice. This article briefly explore these questions, offering what I hope will be useful insights garnered from research and my practical experience.

As it transpires, answering the effectiveness and organisational performance questions is simple. That is to say, high performance requires a great “Culture” and the presence of “Synergy, Trust and Confidence” within and between the board and executive. The absence of these is a predicate to poor performance.

While a board and executive may think they operate well together, identifying the strength and or absence of the critically important blended characteristics and attributes of synergy, trust, and confidence is one of several key outcomes achieved through a behavioural governance review.

Synergy, Trust, and Confidence are derived from a complex blend of the individual and collective characteristics and attributes residing in a board and executives intellectual capital. Intellectual capital is more complex than many think because it comprises four separate yet interlinked capitals:

Individually held:

(1.) Human; innate and learned abilities, expertise, and knowledge, social, structural, and cultural.

(2.) Social; implicit and tangible set of resources available through internal and external social relationships.

Collectively held:

(1.) Structural; explicit and implicit codified knowledge.

(2.) Cultural; identifies the implicit and tangible resources sanctioned through the dominant group (norms, values, and rules.

It is the complex blend of these individual and collective characteristics and attributes derived from intellectual capital that facilitates one critical outcome, the ability of the board to influence the executive, who in turn impact organisational performance. If the blend is right, the outcome is high performance. If not, you get poor performance. This complex interrelationship only occurs in a team environment.

Which brings into stark relief three constants applicable to every organisation. First, the executive is an essential and integrated part of a board's very existence. Second, without the executive, the board as the governing body would be ineffective and unable to fulfil its roles. Third, one without the other is incapable of enabling and then sustaining a high performing organisation. They are intrinsically linked.

For clarity, my definition of the term “executive” refers to the CEO and senior functional managers, e.g., chief financial officer, operations manager, marketing manager, etc., who have regular contact, formal and or informal, with the board and or individual directors.

There are some long held and widely accepted views regarding organisational leadership. Including, organisational leadership comprises two distinct teams: the board and the executive. Each operating independently yet residing within the same organisation. It is correct to say there are two teams (board and executive). But is it correct, as is common, to label the executive as the top team? This label is inaccurate and misleading. While there are two distinct teams, when collaborating, in whatever form that may take, don't they then form another team, the “Third Team”?

My Doctoral research [see: Searching for the “mythical unicorn” the missing link between boards of directors and organisational effectiveness], and more than a decade of advisory practice, supports this view. That organisational leadership comprises three teams, Board, Executive and Third Team. If there must be a “top team” it must be the Third Team [see: The Third Team: Linking Boards and Organisational Performance].

The Third Team forms the last and most critical part of what I call the “trinity of leadership.” The term “Trinity” acknowledges that individually, each team, are unique. Yet the power, and ultimately the performance of the organisation, comes not from their individuality but from their unity as the third-team. When the executive and board understand the power of the Third Team, they realise that while they are individually responsible; they are collectively accountable for organisational performance. This collective accountability when combined with high levels of synergy, trust, and confidence within and between members of the third-team. Creates a culture that permeates the organisation. This culture, based on collective and individual accountability and enabled via synergy, trust, and confidence, drives organisational performance.

As with all teams, it is possible for their performance to be poor or high performing. Organisations recognised as having poorperforming Third Teams include Wirecard, BHS, Greensill Capital, Patisserie Valerie and Carillion. The rationale for the rating is simple: their performance identifies them as poorperforming.

Leading to two questions. First, how can an organisation determine how well or poorly their third-team is performing? Second, having identified how its performing, what steps can be taken to improve or solidify the team's performance?

It is worthy of note that a Third Teams performance and behavioural profile is continually evolving. A single change in its composition can alter the equilibrium, either for the better or worse.

But how will you know if your organisation has a trinity of leadership or a fractured two dimensional leadership? Or, if synergy, trust, confidence, and a culture of mutual accountability are present or simply non-existent?

Identifying and then understanding a third team's blend of characteristics and attributes and their effect on performance requires a different and more nuanced review process. Unlike traditional reviews, a “Behavioural Governance” review evaluates your third teams performance across a range of metrics. Providing the deep insights and breadth of analysis needed to identify how your third team's performance is affecting organisational performance and, importantly, what areas need work.

Before outlining the process used for a behavioural governance review. I will briefly outline some impediments that traditional board reviews face when trying to give insights into what facilitates and drives performance. There are five attributes or outcomes of traditional review processes that are problematical.

(1.) The executive are not included, this is counter intuitive. The executive are the gatekeepers between the board and organisational performance. Not including them in the review means we understand only half the picture.

(2.) The board's collective preference for simplicity and a belief, some might call it arrogance, that only they really know and understand what a board does and how it works best.

(3.) The board and individual directors' aversion to dissonance and ambiguity. This is often seen in their lack of desire to criticise another director's performance, e.g., meeting preparation. A recent PWC survey (2019) found that 50% of those surveyed do not conduct individual assessment of directors. Why, because, of its perceived effect on collegiality, appropriateness, or a general reluctance.

(4.) A deep-rooted belief they operate in an orderly world, which is disconnected from the executive.

(5.) A lack of understanding regarding the importance and affect the individual and collective behavioural characteristics and attributes of the third team members has on the development of synergy, trust and confidence and the flow on effects on organisational performance.

When taking a stakeholder view, reviewing the board in isolation is an attempt to impress the stakeholder that a great deal is being done, when, in reality, little is intended to or will be done. Other common criticisms regarding the outcomes and insights that result from many currently utilised board review practices include:

(1.) They generally exclude outside input.

(2.) They are often viewed as nothing more than exercises in self congratulation.

(3.) They are often based on flimsy methodologies that do little to provide performance or behavioural insights that may lead to improved performance.

(4.) There is little evidence that they do anything more than satisfy a compliance element.

(5.) The outcomes are rarely shared in full with those whose own performance is enhanced or impeded by the board, the executive.

(6.) Lastly and most importantly, they do not shed any light on the levels of synergy, trust and confidence that may or may not exist and how the lack of one or more behavioural elements affects organisational performance.

If your current review process has some or all of the above problems and outcomes, what is its use? Window dressing?

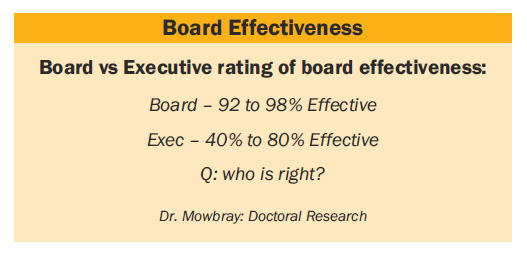

By way of example, one component of a behavioural governance review investigates the board and executives' view of “board effectiveness.” The results are informative, they identify that boards rate their own effectiveness between 92% (lowest) and 95% (highest). Whereas the executive rate their boards' effectiveness between 40% (lowest) and 85% (highest).

Differences in ratings are to be expected. But the degree of difference in the ratings is critical. Typically, in high performing organisations, the variation between a board and the executives' view of boards' effectiveness varies by no more than 20%. This is an acceptable and completely normal variation between views.

Whereas in poorer-performing organisations, the variation between the board and executives' view of board effectiveness is typically 35% or more. This significant difference results from one simple fact. The boards of poorer performing organisations rate their performance as excellent (90-95%). Highlighting a significant problem, board only reviews relying on participant surveys of self assessment are inaccurate.

Experience and results from surveys such as the PWC Board Effectiveness survey show that when a board and executive have widely divergent views of the board's effectiveness. There are diminished levels of synergy, trust, and confidence, which affect performance.

Importantly, it is accepted that the Third Team's performance cannot be mandated via prescriptive codes, policies, or regulations. Equally, enhancing performance begins with understanding the current blend of the Third Teams behavioural and cultural characteristics and attributes. Once known, then a board can discuss the collective and individual strengths and weaknesses from which they can develop a board development plan.

Behavioural Governance Reviews

Compared to traditional reviews, a behavioural governance review uses multiple touch points, combined with observation and interview data. Which facilitates the identification and level of the individual and collective behavioural, procedural, and intellectual capital characteristics and attributes within the Third Teams. The review has four separate yet interlinked components:

(1.) Surveys for both the directors and executive, this collects data on the five key areas.

(2.) Semi structured interviews with individual directors and executive members. The initial interview questions are developed from the analysis of the survey data.

(3.) Observation, attendance at board meetings. 4. Review of structural elements, annual board plan, succession planning, policies, etc.

The above systematic approach tests five critical areas. Each is a key indicator for determining if the Third Team's performance will either inhibit or enhance organisational performance.

(1.) Do directors enjoy working in a cognitively challenging environment?

(2.) Is the intellectual capital (human, social, cultural, structural) of the board a good match for the organisation?

(3.) Do the executive make use of the tacit and explicit knowledge of the directors through the replication, innovation, or adaptation of this knowledge?

(4.) What is the state of the board–executive relationship?

(5.) What is the degree of disparity between the board and executives view of the board's effectiveness?

The depth of analysis provided via a behavioural governance review gives organisations the depth and breadth of insights needed to take a truly collaborative and measured approach to improving performance and effectiveness that is not possible with other forms of review. The review provides the benchmarks on which an organisation can develop a well structured and resource plan for the continuing education and structured succession planning required in today's fast moving environment.

When repeated, a behavioural governance review provides a window through which the effect of changes can be measured. Providing a clear measurable analysis of the Third Team's improvement or decline in performance. This is something that every stakeholder desires.

While a board and executive may think they operate well together, identifying the strength and or absence of the critically important blended characteristics and attributes of synergy, trust, and confidence is one of several key outcomes achieved through a behavioural governance review. As humans, we are adept at hiding or glossing over our own or our team's shortcomings, especially if our reputation or livelihood may be put at risk. Fortunately, or unfortunately, depending on your point of view, these charades cannot be maintained or hidden from a behavioural governance review.

Until organisations incorporate behavioural governance reviews as part of their performance monitoring programme. Organisations and their stakeholders will be 'boxing the wind' as they try to understand if their board is effective or just believes it is.

Back to Home

Back to HomeAuthor

Dr. Denis Mowbray FCG FGNZ

He is a Director and Fellow of 'The Chartered Governance Institute' and 'Governance NZ.' He is also President and Chair, Governance New Zealand Inc, and Director, Gryphon Management Consultants. His influential work on “behavioural governance”, and his identification of the 'Third Team' are key platforms of his work with boards and directors. He is a specialist working in the corporate and not for profit sectors, specialising in governance, strategic development and organisational change. He has a thriving consultancy practice specialising please visit: www.gryphonmanagement.com.

Owned by: Institute of Directors, India

Disclaimer: The opinions expressed in the articles/ stories are the personal opinions of the author. IOD/ Editor is not responsible for the accuracy, completeness, suitability, or validity of any information in those articles. The information, facts or opinions expressed in the articles/ speeches do not reflect the views of IOD/ Editor and IOD/ Editor does not assume any responsibility or liability for the same.